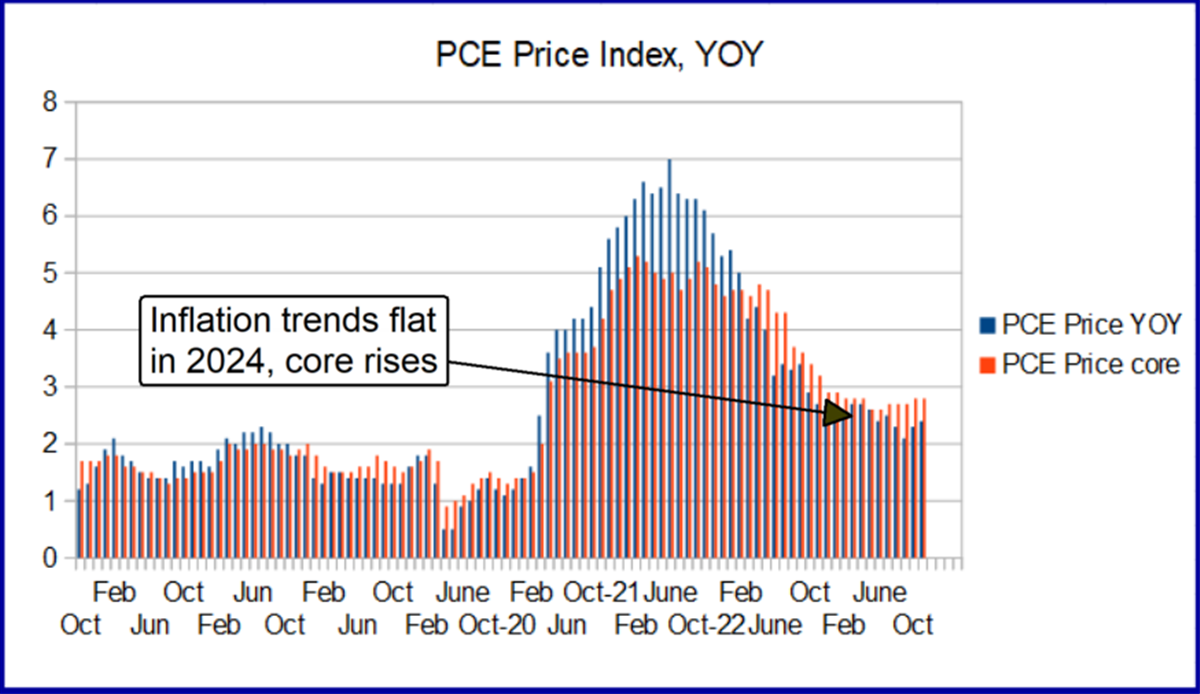

The market continues to price in the possibility of a rate cut in 2025, which could be a big mistake. Despite inflation falling from COVID highs, it remains hot and uncooperative. Even if data for January and February are weaker than expected, the inflation trend remains flat, not downward, and does not correspond to the idea of lower interest rates. Other factors pointing to higher interest rates include labor markets, consumer spending, oil prices, GDP expectations and the 10-year Treasury note. This is a look at why.

Fed mandates are not balanced

The Fed’s mandate is twofold: support the economy while protecting the labor market and keeping interest rates low. The trend in the inflation data is undeniable: it is not cooperating, and the trend in the labor data is one of the reasons. The labor market has cooled from its 2022/2023 peak. However, the country remains healthy, strong and resilient, with new jobs averaging 191,000 in 2024, unemployment averaging 4%, wage growth 4%, plenty of jobs and historically low job applications. unemployment benefits.

Some warning signs include Challenger, Gray and Christmas data on layoffs and hiring plans, as well as data on total jobless claims. However, even these are better than they appear at face value, demonstrating volatility in a changing labor market environment rather than deteriorating conditions.

Consumer trends in 2024 are equally strong. Their average growth is expected to be more than 3% compared to the previous year. This is enough to outpace the rise in core consumer inflation relative to the PCE price index, showing a slight increase in demand. The 2025 forecast calls for retail sales to increase to 3.5% or higher, adding upward pressure on prices, and could develop tailwinds in the second half of the year as Trump’s policies take effect. Coincidentally, the FOMC noted the same fact at its last meeting.

Rising oil prices: will contribute to higher inflation in the first quarter

Oil prices exacerbate inflation by affecting the cost of resources at every level of the system. The price of oil fell in 2024, hitting a long-term low in the fourth quarter, but then rose strongly. It was 17% below its mid-January low, as evidenced by price action and indicators including moving averages, stochastics and MACD. WTI, trading around $78.25, is at the midpoint of its multi-year trading range and has plenty of room to rise. The bottom line is that oil prices will drive inflation in the first quarter and potentially throughout the year, assuming no price correction occurs.

The CME FedWatch Tool, a gauge of Fed odds based on futures contracts, still suggests cuts are likely in 2025, but the odds are falling sharply. In his opinion, the reduction is unlikely to occur before July, and the reduction before the end of the year is in question. At 75%, it won’t take long to cement the idea of no cuts this year in the market’s mind, and that event will likely lead to a stock market correction. The good news is that the S&P 500 NYSEARCA: SPY the correction is unlikely to lead to a sustained decline due to underlying economic health driving higher inflation.

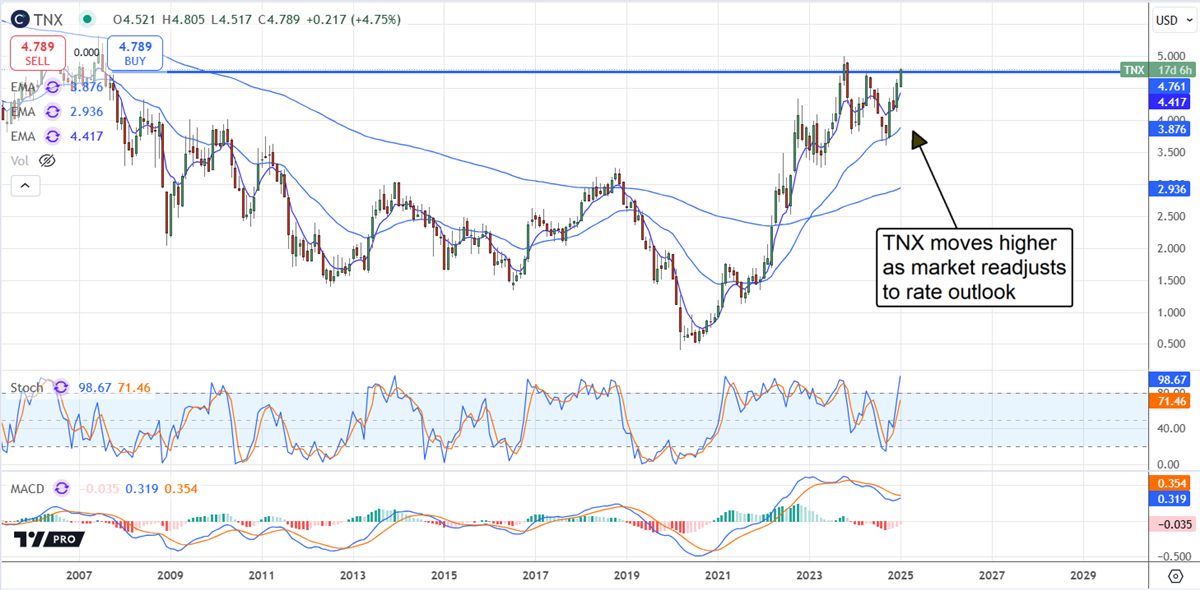

10-year Treasuries adjust to better-than-expected conditions

The 10-year Treasury yield is rising and in line with the FOMC’s changing forecasts. Yields have risen significantly in the first two weeks of the year, rising to an 18-month high supported by the short-term 30-day and long-term 150-day EMAs. Yields are likely to continue rising as the 4.8% spread over the FOMC’s expected year-end benchmark rate of 4% is well below the long-term average. In such conditions, yields could rise by another 40 bps. or more before reaching its maximum level, and the Fed’s rate cut to 4% is doubtful.

Before you consider the CBOE Volatility Index, you should hear this.

MarketBeat tracks Wall Street’s top-rated and best-performing analysts daily and the stocks they recommend to their clients. MarketBeat identified five stocks that top analysts are quietly whispering to their clients to buy now, before the broader market takes hold… and the CBOE Volatility Index wasn’t on the list.

While the CBOE Volatility Index currently has an analyst rating of Hold, the top-ranked analysts think these five stocks are Strong Buys.

View five stocks here

Which stocks are most likely to thrive in today’s challenging market? Click the link below and we’ll send you MarketBeat’s list of 10 stocks that will rise in any economic environment.

Get this free report