Defense shares are returned after messages about the first quarter from Lockheed Martin NYSE: LMTNorthrop Grumman NYSE: Noand RTX NYSE: RTXThe field of the main reason is the uncertainty, which follows a cool leadership. As for uncertainty, companies are faced with unknown effects of tariffs that may affect their profitability. This is a risk that cannot be ignored.

Each company confirmed its forecast for 2025Calling growth and sufficient cash flow to maintain financial stability, reinvestment in the operation and return capital to shareholders.

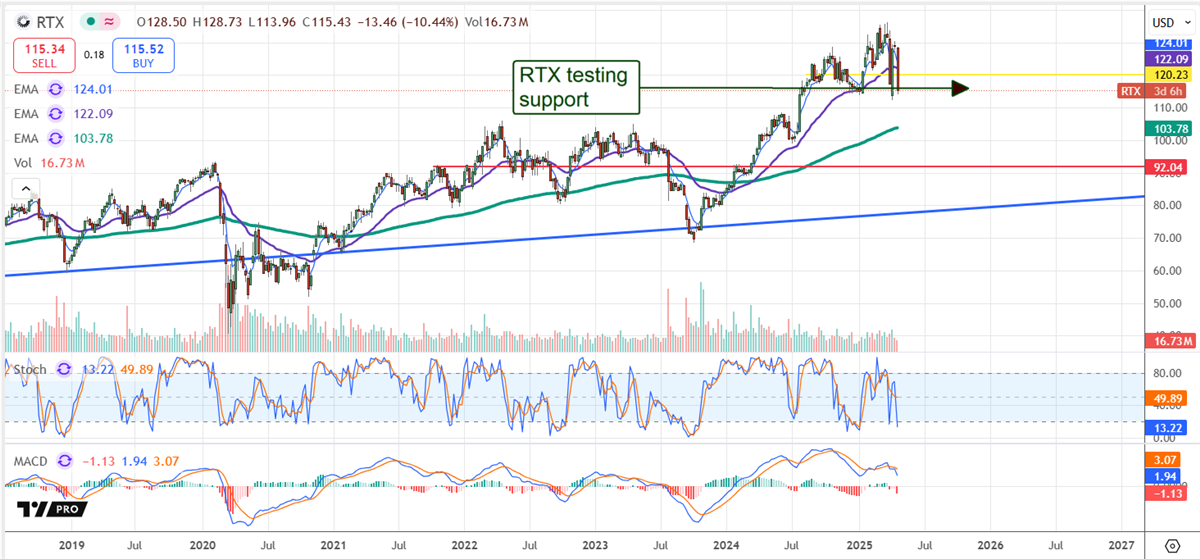

RTX: solid results with long -term growth

RTX today

As of 25.04.2025 203: 59

- 52-week range

- $ 99.07

▼

$ 136.17

- Dividend yield

- 2.01%

- P/e ratio.

- 35.33

- Value is valuable

- $ 161,38

RTX is outstanding in the first quarter. He surpassed from above and the result, with an increase in profit by 10%, due to force in key segments, such as drones and unmanned equipment. Margin News is also good, and the leadership was confirmed.

His ransom did not compensate for diluted actions in the first quarter, but they do over time. The profitability of capital remains the main part of the history.

Clearly continues to grow, and new contracts win, adding to an already durable pipeline. Analysts see the most potential value here, for the purpose of Marketbeat consensus, to be predicted to 40% of profit. Nevertheless, the potential will probably be limited in 2025, until it becomes greater clarity in the perspective of the tariff.

Lockheed Martin: Consistent performance

Lockhid Martin today

Lockhid Martin

As of 25.04.2025 203: 59

- 52-week range

- $ 418.88

▼

$ 618.95

- Dividend yield

- 2.76%

- P/e ratio.

- 21.47

- Value is valuable

- $ 544.79

Lockheed surpassed income and income in the first quarter with an increase in profit by about 15%. The force was wide, but especially strong in unmanned systems. The space remains a weak place, but not enough to disrupt history.

The profitability of the capital of Locheis was significant. Buyers reduced the number of shares by 2.6% per quarter, and dividend profitability is 2.9%, which is the highest of the group. The payment is well covered and expected to grow.

The lack of healthy, adding $ 485 billion for orders to the collective sector – 10 quarters income at the current pace. The volatility is low, and the institutional percentage remains high in the 2nd quarter.

Northrop Grumman: weakness at a price?

Northrop Grumman today

Northrop Grumman

As of 25.04.2025 203: 59

- 52-week range

- $ 418.60

▼

$ 555.57

- Dividend yield

- 1.74%

- P/e ratio.

- 16.70

- Value is valuable

- $ 545.31

Miss Q1 Northrop was tied to the expected disclosure of operations related to the space and increase costs in the B-21 program. Despite this, the company confirmed its leadership, predicting annual growth with expansion in all segments, including space.

Buyers were more significant than peers, reducing the number of shares by 3% per quarter. Dividend yield is the lowest at 1.5%, but also the safest, with a payment coefficient of about 35%. Capital profitability is well supported and expected to grow.

Donations influenced the margin, but there was not enough to change the financial health of the company. Consulting signatures increased, and the ratio of the book to Bill remains strong.

Sector picture: under pressure, but retention

The defense had a solid Q1 in general, despite some spotted disadvantages and sales exposure. The key detail is that diversified business models – balancing private and state contracts – support operations. Everyone registered force in critical segments, including drones and unmanned equipment, with a space worthy of attention, in all directions.

Cleaned is a critical factor. Everyone reported the winnings of the contract and the growth of the lag, including record levels for some. The conclusion is that the collective, approximately $ 485 billion, corresponds to 10 quarters of income at the first pace, providing sufficient visibility.

Analyst and institutional trends remain positive

Analysts of trends support defense stock markets in 2025, including an increase in coating, stable or strengthening moods, as well as stable or strengthening consensus price purposes. Consensus price target indicators reported by the MarketBeat Minimum forecast, double -digit increase for these shares, in the range from 20% to 40%.

Similarly, institutional trends also support defense actions in 2025. These trends include a high level of ownership, aggravated by long -term high activity in the first quarter and purchase in the second quarter. Assuming that these trends continue, these shares are unlikely to fall much further in the second quarter and may begin to bounce before the start of the second half.

Among the catalysts is Trump’s promise to increase defense costs in 2026 by as many as 12%to ensure the unrivaled military force of America. In addition, the president continues to strive to increase expenses by NATO countries.

The volatility, or its absence, is another reason why protective shares are good purchases in 2025. These shares are traded on a significantly lower beta version than the S&P 500, providing some isolation from everyday market movements and a sharp, wide market reduction.

Before considering Northrop Grumman, you will want to hear it.

Marketbeat monitors the highest and most effective analysts with the most effective Wall Street analysts and promotions that they recommend to their customers daily. Marketbeat has identified five shares that leading analysts quietly whisper to their clients to buy now before the wider market wins … and Northrop Gramman was not on the list.

While Northrop Grumman is currently a moderate purchase rating among analysts, analysts with the highest rating believe that these five promotions are better buying.

View five shares here

Discover the 7 best shares of AI in which they now invest. This exclusive report emphasizes the company, heading the AI revolution and forming the future of technology in 2025.

Get this free report