From meme stocks and cryptocurrency to special purpose acquisition companies and initial public offerings, the last few years have proven that investors will jump at risky opportunities if there’s a chance of getting rich quickly.

But for every investor who profited from GameStop’s stock surge or the rise of dogecoin, there are many, many more who lost out. They experienced first-hand that while investing can be exciting, it probably shouldn’t be. In fact, some of the most successful investing strategies over the long term are pretty boring.

But sticking to the basics — like index fund investing, dollar-cost averaging and dividend reinvestment plans — is proven to slowly build wealth over time, even if it’s not as flashy as going all in on a stock right before it skyrockets. So here are some of the most boring (and effective) ways to become a millionaire.

No. 1: Index fund investing

Picking stocks can be fun. And if you choose the right ones at the right time, it can also be lucrative. But timing the market is exceptionally challenging, even for the pros.

The Wall Street Journal’s Jason Zweig recently analyzed data from research firm Morningstar and found that in the first half of 2024, 81.8% of actively-managed funds failed to outperform the S&P 500 index. Going back a decade, nearly 73% failed to do so.

“When you pick stocks … you’re displaying confidence that you somehow have knowledge that the rest of the market didn’t bake into the price of an investment,” says Brenton Harrison, a financial advisor and founder of advisory firm New Money, New Problems. But opting for index funds — baskets of securities that aim to mimic an index like the S&P 500 or Nasdaq Composite — means you don’t have to choose.

These funds allow you to spread your investments out, increasing the chances that if one sector of the index struggles, another will hold up. That’s the power of diversification, which index fund investing provides all in one place. For example, the SPDR S&P 500 Trust (SPY) gives investors weighted exposure to all 500 companies in the index in a single fund.

Over the past 30 years, the S&P 500 has an average annual return of 10.52%, while the tech-heavy Nasdaq Composite — albeit more volatile — has returned 10.9% over the past 20 years. Funds tracking these indices have amassed an impressive track record. The aforementioned SPY has gained 1,180% since its inception on Jan. 29, 1993, while the Fidelity NASDAQ Composite Index ETF (ONEQ) has gained 823% since debuting on Oct. 3, 2003.

No. 2: Dollar-cost averaging

If you contribute a portion of each of your paychecks to a 401(k) plan, you’re already using this simple strategy for building long-term wealth. Dollar-cost averaging is a technique that involves investing a set amount of money at regular intervals, no matter what is happening in the market at that time.

While the ideal investing strategy is to buy when prices are low and sell when they’re high, timing the market is extremely difficult. Last December, Morningstar analysis showed that over 21 years, buy-and-hold portfolios outperformed market-timing portfolios by 10%. Additionally, while market-timing investors would see higher returns by putting money to work in the market when stocks were cheap, those returns were more than offset by losing out on returns from holding cash back when the market was overvalued.

That’s because investing at regular intervals removes some of the risk of that opportunity cost. “Dollar-cost averaging is one of the best financial tools that a person can use because it takes human error out of the investing process,” Harrison says. “Instead of you feeling like you have the ability — which we don’t — to time the market, it gives you the best opportunity to get the best cost for your investment.”

No. 3: Dividend reinvestment plan

The key to exponentially growing your wealth is compounding returns, or gaining returns on your returns. It’s so powerful, Albert Einstein referred to it as the eighth wonder of the world.

One way to take advantage of this compounding is by setting up a dividend reinvestment plan. Shortened to DRIP, this entails automatically reinvesting any dividends you receive from stocks or funds that you own.

“Dividend reinvestment is an easy way to have something where it’s building upon itself,” Harrison says. Enacting a DRIP means you’re increasing the force that your account is growing with.

Here’s a hypothetical from Charles Schwab that shows the power of this strategy: A $100,000 investment made in 1990 in a fund tracking the S&P 500 would have grown to more than $2.1 million by the end of 2022 if dividends were reinvested. Remove that dividend reinvestment? That same investment would have only grown to $1.1 million — or just over half as much.

The proof is in the pudding

When combined, these three strategies — index fund investing, dollar-cost averaging and dividend reinvestment — are capable of producing eye-catching results over the long term.

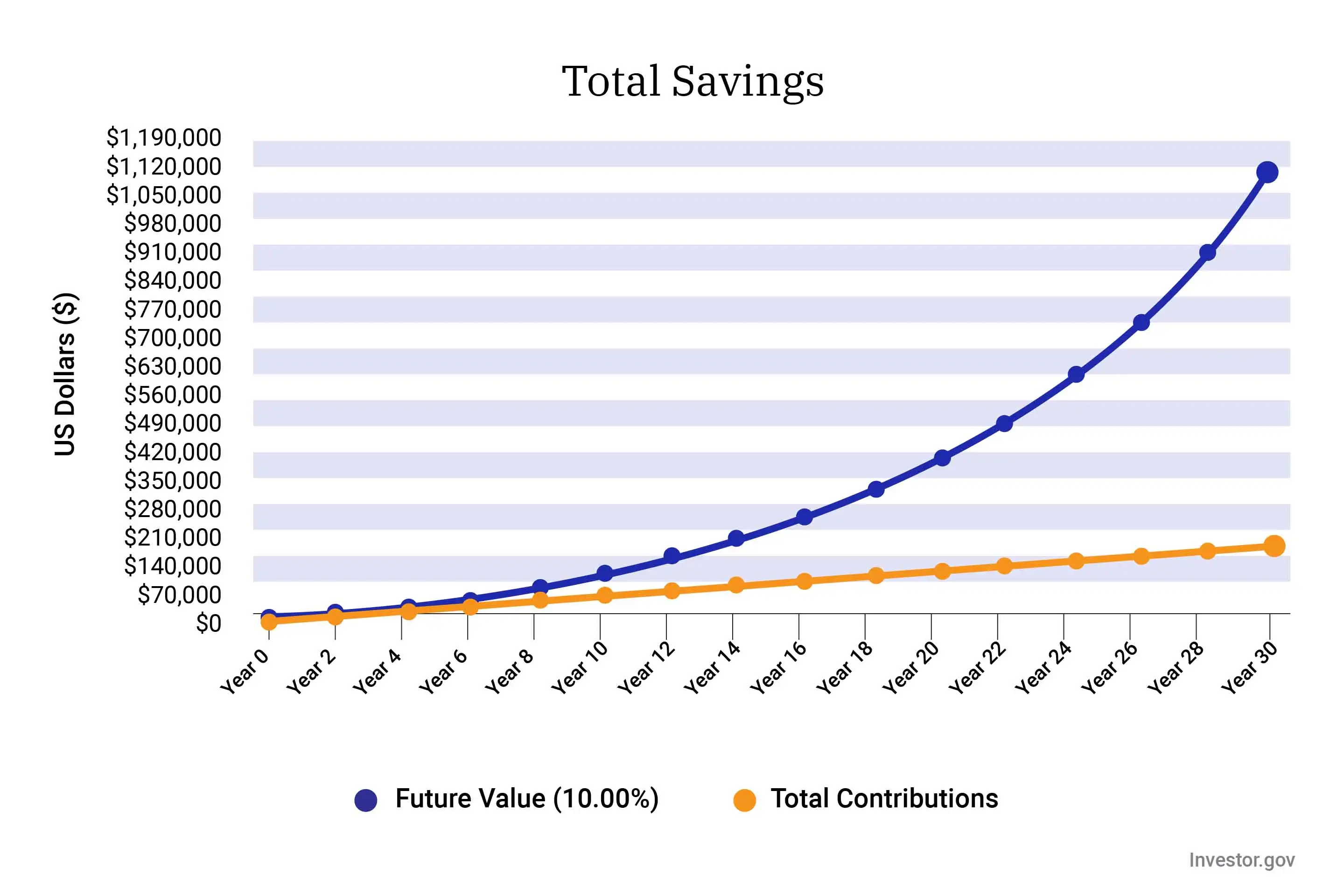

Let’s say you invest $500 every month (or $125 each week) in an index fund with a compound annual growth rate of 10% — slightly less than the average annualized return of the S&P 500 over the past three decades — and that fund pays a quarterly dividend. According to a calculator provided by the U.S. Securities and Exchange Committee, in 30 years, you’ll have amassed over $1 million:

Specifically, using the three previously mentioned strategies to invest $180,500 over 30 years would produce an estimated $1,111,168.06.

Is it boring? Yes. But is it effective? Absolutely.

These are proven strategies that are far less risky than speculating on meme stocks, crypto or other high-risk assets. And if you stick to the plan, your future self will thank you (while hopefully sitting on $1 million).